Notes On The Commodity Supercycle & Tungsten

A look into one of the more interesting commodities out there

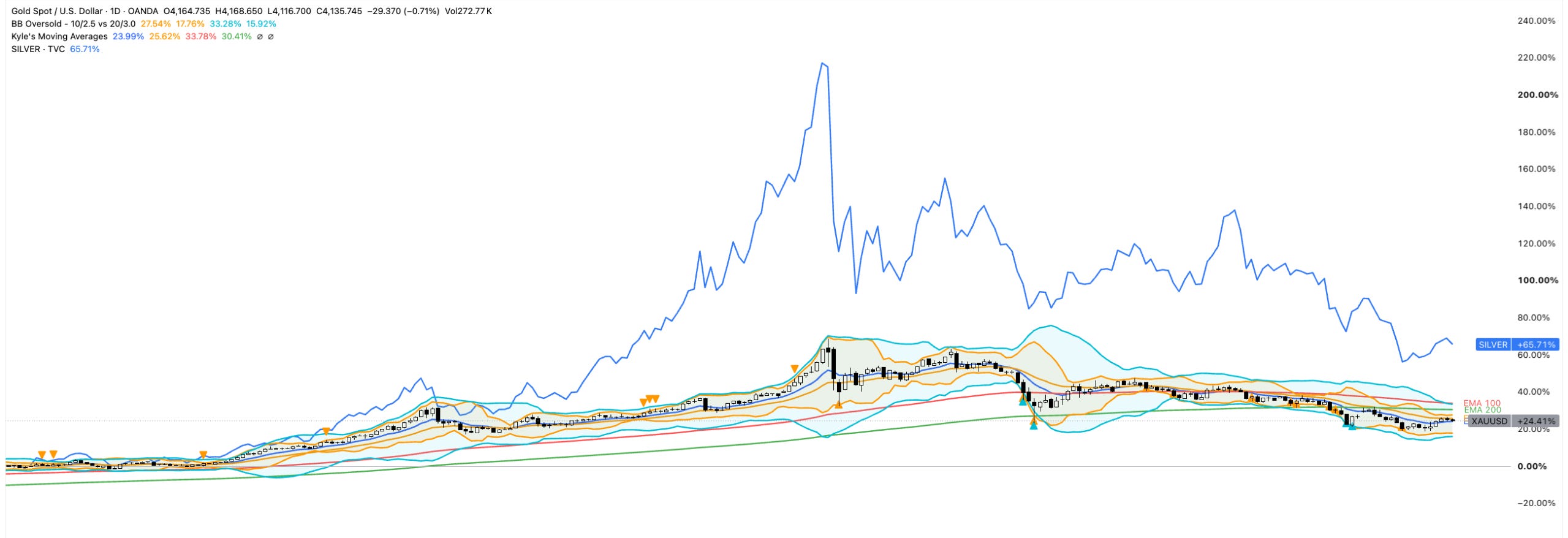

Gold and Silver saw a meteoric rise in the past 1Y but has since corrected sharply, with both experiencing sharp double digit declines since their tops. The “Commodity Supercycle” that was once upon us seems to have boiled over - I remember that during those periods, people were longing Copper (Copper wiring was used ubiquitously in the construction of data centres), Platinum (Deficit Story), Zinc, Aluminium, etc.

And earlier this year, we had “Commodity Supercycle v2” - this time with the closure of the Straits of Hormuz, it was believed that we would face a shortage of oil, and combined with weather factors (El Nino), and the fact that a lot of fertilizer was shipped through the strait (fertilizer stocks saw a sharp knee-jerk reaction upwards, with names like CF up ~70+% at peak prices) , we would be lacking in corn and wheat in harvesting season this year.

There are a few things to note here. Firstly, it is true that we are in a shift from bits to atoms - from software to hardware. The main driver has been AI - with the semis-buildout in full force. But beyond this, we have protectionism measures in place as the US aims to rebuild its manufacturing capacity, reshore talent, and become self-sustaining once again. All of this has led to an increased demand for all sorts of assets, which eventually trickles downstream to the raw materials themselves.

It is also true that, in the markets, neither of these “Commodity Supercycles” turned out to be long lasting at all - as you can see above, many of these eventually came down to reasonable levels after the crisis passed. They were all one “large basket trade”, with the metals like Platinum, Zinc and Aluminium all closely tied to supply deficits meeting new demand; and once that demand had been met, they repriced sharply.

However, I do not think it is over. I believe that it makes sense to position for Supercycle 2.0 - this time, less like a single unified boom, and more like a fractured set of separate cycles. The main factors are still in play - deglobalization, AI, and energy transition are driving a broader, longer lasting cycle, with supply constraints from years of underinvestment. However, it is important to pick the right commodity, because each have their own respective reasons for going up / down. In reality, many of these should be treated as separate assets in the market.

Gold, as the prime example, had monetary / macro drivers with central banks around the world buying and de-dollarization being a core focus early in the year. With the original thesis hinging on lower rates, higher fed liquidity and Trump instability, gold was a safe haven for investors to protect themselves from uncertainty. However, these factors have all inverted - rates are now expected to hike, fed liquidity has been lowered, and Middle Eastern countries such as Turkey have been selling with what’s going on in that part of the world.

Silver rode gold’s coattails but with an industrial twist - the market also moved on the fact that there would be a large deficit for silver, due to it being needed in AI, photovoltaics (solar), and the electrification of the vehicle fleet. There was also a period where there was supply tightness, where delivery demand could not be met by normal means.

This same reasoning can be repeated for every commodity out there. Each one has their own idiosyncratic driver beyond the general “metals / agri / etc.” basket that they’re normally grouped with. And so, with the help of AI, I have filtered the universe of commodities and landed on some that I like. My view of the commodity supercycle, and the conditions something has to meet to belong in it, is as such:

The commodity supercycle will be bifurcated, not broad. There is already a fracture into distinct micro-markets where a handful of commodities have structural tailwinds, and the rest trade on their own idiosyncratic supply/demand and cyclical forces.

The character has changed - it is a multi-driver cycle which makes it more durable but harder to time. The old cycle had clean narratives (Chinese industrialization) and had one clean endpoint. This one is powered by multiple factors - energy transition, AI, defense re-armament, de-dollarization, reshoring of manufacturing capacity, etc. and a given commodity can be pulled more than one at once. This makes winners more durable, but also with no single demand engine, there’s no obvious bell to signal the top, or even when it’ll come into play

Just because there’s a structural floor doesn’t mean there’s no drawdown. The past few months of watching Gold / Silver / Metals + Iran War situation has shown me that the path is extremely volatile - the highs are much higher than usual, yet the boom-bust nature of commodities mean that one has to be adamant in taking profit.

TLDR: Like everything in investing, selection, and timing, is everything.

Tungsten

The commodity that I have landed on is tungsten. To be honest, the AI gave me 5 commodities based on the factors of: 1) Genuine multi-year structural story; 2) A real public way to bet - either liquid futures / physical, or an investable producer ; and it landed on: Copper / Uranium / Tungsten / Silver / Gold.

I thinned the list to Uranium & Tungsten simply because I believe they offer more asymmetric opportunities intuitively. Gold, Silver and Copper are all so large and widely covered that I believe it comes down more to market timing more than anything, to figure out when they’re prime. The path that they have taken thus far (Gold from ~3k > ~5k > ~4k, for example) necessitates trading around it. They also, in their own way, have already “pumped”, and the conditions for continuation does not seem ripe at the moment. Hence - timing.

Uranium is something I hope to cover in future notes RE: Nuclear. And with those out of the way, we’re left with Tungsten. Before we continue, I would like to highlight that much of this was AI generated through multiple sources, and there may be inaccuracies in the figures mentioned. As much as possible I tried to fact check these, and many of these points are taken from trustworthy secondary sources to improve reliability. But at the end of the day, I am just a monkey with access to Machine God Intelligence, and these are just my notes. Moving on.

Some notes on what Tungsten is and does:

It has the highest melting point of any metal (~3422 celsius), has extremely high density, and exceptional hardness, which makes it ideal for use in industrial tooling, aerospace components, military projectiles, etc. This also makes it hard to substitute - few materials can replicate this without performance loss

It is extracted mainly from two ores - wolframite and scheelite - and then refined into intermediates (Ammonium Paratungstate , Tungsten Oxide, Carbide Powder) that feed into the end products.

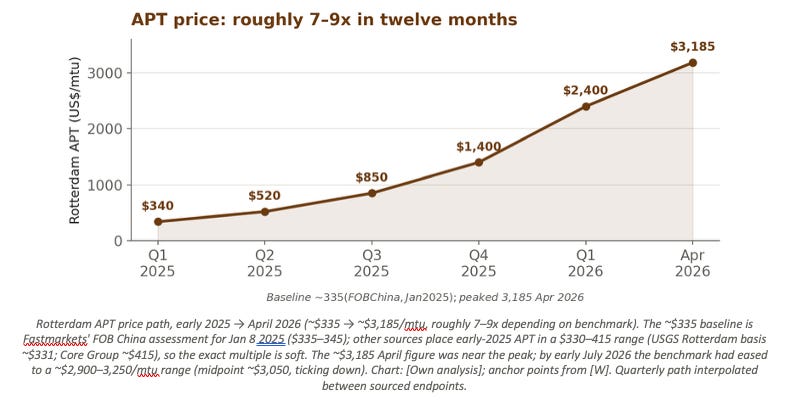

The benchmark intermediate - ammonium paratungstate (APT) moved from roughly $340/mtu in early 2025 to a peak of $3,185/mtu in April 2026 and sits near $3,185/mtu as of early July 2026

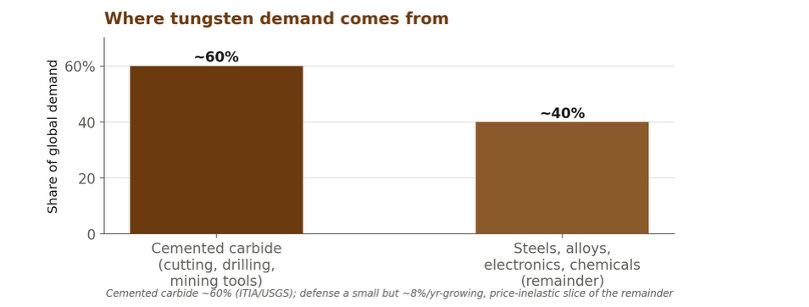

Tungsten is used the most in the following applications:

Cemented carbide tooling (~60% of demand): Cutting tools, drill bits, and mining/construction inserts. Hardness and wear-resistance let them machine steel at high speed; ceramics, PCD, and CBN substitute only in specific niches, usually at a performance or cost penalty.

Defense & munitions: Density and hardness make it ideal for armor-piercing rounds, kinetic-energy penetrators, missile counterweights; A single guided-MLRS rocket carries ~50 kg of tungsten.

Aerospace & superalloys. Heat-resistant alloys for jet engines, turbine components, and rocket-engine nozzles that must survive extreme temperatures.

Semiconductors. High melting point, inertness, and adequate conductivity make it useful for filling nanoscale connection gaps via chemical vapor deposition (WF₆).

Photovoltaic wire. Tungsten wire increasingly replaces carbon-steel wire for slicing silicon wafers - a thinner wire wastes less silicon per cut, a fast-growing new demand vector.

Demand / Supply Analysis

The heart of the thesis is that Tungsten runs counter to the demand outstripping supply thesis - it is a supply-led deficit, colliding with growing demand in a market where new supply takes years to build.

Demand Side

Cutting / carbide tooling is steady-state and hard to substitute. (Note: tungsten-carbide market reports often name automotive or mining/construction as the single largest end-user vertical; that is the same demand sliced by downstream industry rather than by first-use application)

Substitutes (ceramics, PCD, CBN, moly/niobium carbide) exist but mostly reduce rather than replace tungsten, usually at a performance or cost penalty.

Defense: A modest share of volume (~12% of the market today) but growing ~8%/year as stockpiles rebuild. Governments are price-inelastic customers that do not defer munitions procurement just because it got expensive.

Semiconductors & PV (high CAGR): One demand model runs semis and solar at ~15% CAGR, everything else ~5%, yielding ~77% demand growth over a decade. Two real drivers underneath: tungsten hexafluoride (WF₆) for filling nanoscale contacts in chipmaking, and tungsten wire replacing carbon-steel wire for slicing silicon wafers (thinner wire = less silicon wasted). Both are new demand curves that barely existed a few years ago.

DFARS Anchor - From Jan 1 2027, US defense procurement bars tungsten whose supply chain touches China / Russia / North Korea / Iran with traceability to the mine - forcing Western defense buyers onto a supply base that barely exists yet.

Emerging / long-dated optionality: Lithium-battery cathode additives, and - as a wildcard - plasma-facing walls in fusion reactors (one estimate: ~250 t/reactor/yr, which at scale could rival China’s entire current output). Scenarios, not forecasts, but they skew the long-term demand risk to the upside.

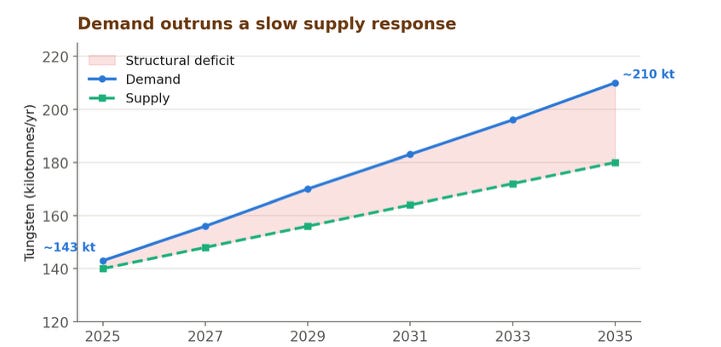

The aggregate: demand is forecast to rise from ~143 kt (2025) to ~210 kt by 2035 — roughly 47% growth (Canaccord). The point isn’t just the size of that number; it’s that the growth is concentrated in the vectors least likely to walk away when prices rise.

Supply Side

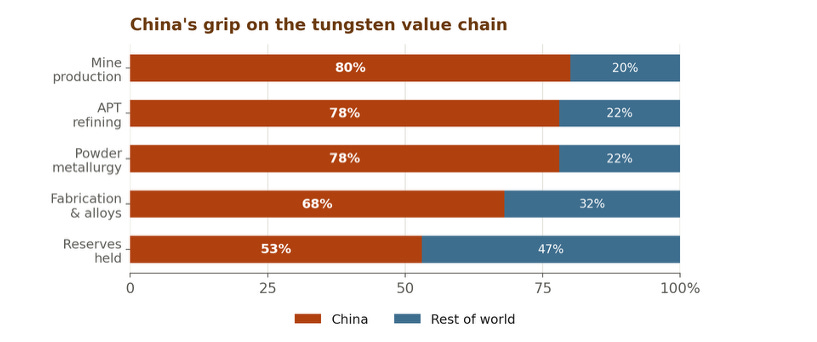

Extreme Concentration: Roughly 80 - 85% of global mining production originates from China, and an even larger share of downstream processing is owned by them. China mined ~67,000 of the ~78,000 tonnes produced globally in 2025 - roughly 86%, and controls ~70–85% of every downstream processing stage (USGS). This exceeds even rare earths, where production has gradually diversified.

This was converted into leverage - from Feb 2025 there was export licensing on Ammonium Paratungstate and intermediates and was halted entirely, before resuming ;

From Dec 2025 it restricted tungsten export to only ~15 approved companies.

Geographical Depletion: Chinese mined production reportedly fell ~10% YoY to ~61,000t in 2025 on aging mines (some 30+ years old), declining ore grades, and environmental clampdowns; the national mining quota was cut ~6.5%.

No Supply In The Rest Of The World: The deficit persists because supply cannot answer quickly. The US has had no commercial tungsten mine since 2015, and tungsten mines typically need 5–8 years from discovery to production due to complex permitting and the specialized metallurgy of low-grade, multi-phase ores.

A second dependency compounds it: much refining capacity for intermediates still sits inside China, so even ex-China mines may rely on Chinese processing

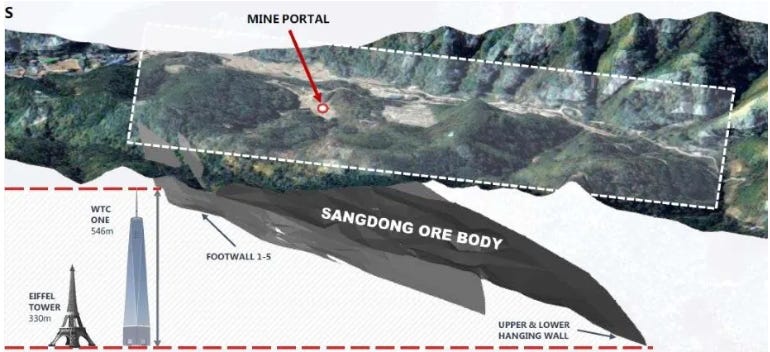

Almonty’s Sangdong (South Korea) is the newest non-Chinese addition - as of July 1, 2026 it crossed from development into revenue production. However, this is new and will take time to start up.

The Balance

Putting the two together, a structural deficit emerges that should persist while supply grows slowly off a non-Chinese base. Demand climbs ~47% to 2035 while supply lags, pointing to a persistent deficit through at least 2030.

The gap is wide and slow to close: demand ~143kt → ~210kt by 2035 (Canaccord), against a non-Chinese supply base starting near zero. Even if every planned Western project delivers, the incremental tonnes are modest against a ~130kt market.

Supply is structurally late: 5–8yr mine lead times, no US mine since 2015, and much refining still inside China mean the response lags the deficit by years, not months.

New supply is real but small: Sangdong now producing (~2,300t/yr, Phase 2 ~2027), plus Barruecopardo, Mt Carbine, Hemerdon, Mactung - helpful at the margin, not gap-closing.

Recycling caps the upside, doesn’t fill the hole: ~25–35% of demand is met by scrap, but it only ramps after prices stay high for a while - a lagging release valve.

Honest caveat: the deficit’s size varies by forecaster (CICC ~20,000 MTU by 2028; others larger). The direction is well-sourced; the exact annual tonnage isn’t gospel.

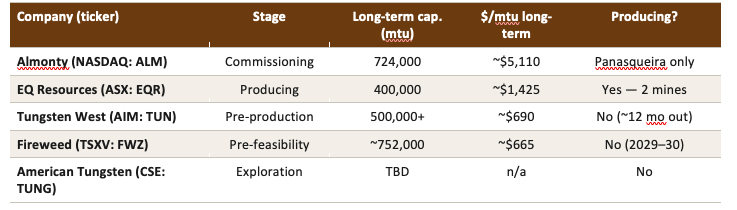

Expression Of The Trade - ASX: EQR

With no futures contract and no physical ETF, exposure runs entirely through a small, illiquid bench of listed miners. My personal favourite is ASX:EQR.

Bull

A real producer, not a promise: only multi-mine Western producer actually selling concentrate - FY2025 output 1,678t WO₃ across Mt Carbine (Australia) and Barruecopardo (Spain).

Revenue inflecting hard: FY2025 revenue A$66.1M, up 146% YoY, with five offtake contracts worth ~US$124M over 24 months - real visibility, in DFARS-friendly jurisdictions.

Enormous operating leverage: at spot prices and its ~3,350t/yr target, the forward multiple is only ~2x EV/EBITDA (my math: ~1.8x on ~A$1.4B EV vs ~A$800M modelled EBITDA). If tungsten stays high and production ramps, it’s cheap.

Bear

It loses money today: FY2025 net loss A$39.2M (total comprehensive loss), negative group EBITDA, ROE ~−97% - so that "2x" is a forward, best-case figure, not what it earns now.

The ramp is a doubling, not a given: the 2x needs production to roughly double from 1,678t to ~3,350t and spot prices to hold. Miss either and the multiple blows out.

Balance sheet is stretched: net debt ~A$85M (70% gearing), current ratio 0.24 — a net working capital deficit of ~A$97M - and operating cash flow of −A$16.9M. It’s still funding itself through raises (shares +35% YoY = real dilution).

Illiquid and already run hard: stock up ~500%+ in a year;

Bear Cases

And like I mentioned earlier - each commodity has their own idiosyncratic drivers, and in this case, Tungsten could quite easily reverse just as Oil did after the SoH tensions eased. In this case, we have:

Policy reversal: The biggest swing factor is Beijing. Resumed APT exports could deflate the political premium faster than a geological deficit would; structural NATO demand limits the depth but not the fact of a sharp correction.

It is a cyclical commodity first: Industrial demand dominates; a manufacturing recession historically pulls tungsten down hard.

Recycling & stockpile release. At these prices, scrap recovery and strategic-inventory drawdowns act as moderating forces.

Thin liquidity, no hedge. No futures complex means thin price discovery and two-way volatility; junior positions gap on financing events. Hence, position sizing matters.

Substitution over time. Few effective substitutes today, but sustained high prices incentivize thrifting and R&D into ceramics/alternative alloys - a slow, long-term risk.

Tungsten is the cleanest already-realized supply-shock in the critical-minerals complex: irreplaceable in its core uses, extreme supply concentration weaponized by export policy, real geological depletion, a defense deadline, and a supply response measured in years. The setup is structurally bullish and expects deficit through ~2030.

The honest counterweight, best put by the one skeptic, is that this remains a thin, unhedgeable, cyclical market where the same leverage that powers the upside powers the drawdown - and the only public expressions are small miners carrying execution and financing risk on top of the commodity view. The thesis is real; the path will not be smooth; and “structural” describes the multi-year floor, not protection from a violent correction along the way.

Resources

Reports & sources I referenced when writing this.

Memory Vs Tungsten By Le Shrub

The Comprehensive Industry Analysis of Tungsten and Tungsten Market by AT Investment Research

Claude By Anthropic

Gemini By Google

Disclaimers

This article is personal research and commentary for informational and educational purposes only. It is not investment advice, financial advice, or a recommendation to buy, sell, or hold any security, commodity, or instrument. I am not a licensed financial advisor, and nothing here is tailored to your circumstances, objectives, or risk tolerance. Do your own research and consult a licensed professional before making any investment decision.

Portions of this piece — including data, figures, and price levels — were compiled with the assistance of AI tools (Claude, Gemini) drawing on multiple secondary sources. Figures are approximate, may contain errors, and were fact-checked only on a best-effort basis. In particular, prices, company financials, production figures, deficit estimates, and forward multiples should be independently verified against primary sources (company filings and named research providers) before being relied upon. Estimates and forecasts cited belong to their respective authors and are subject to change.

I may hold positions in the securities or commodities discussed. I may buy or sell at any time without notice. Past performance and prior price moves do not indicate future results. You alone are responsible for your investment decisions.